The Polar Report #2

Welcome to The Polar Report, a curated view of what is happening in the world of digital Monetisation, Audience Development, and Measurement. This week we dive into Facebook’s latest brand safety tools, contextual targeting in CTV advertising, metrics, and more!

Monetisation

177 Media Agencies Claim 37% of YouTube Ads Could Be Unsuitable

A recent article on AdExchanger discusses the evolution of brand safety, specifically how YouTube and CTV have helped improve brand suitability and how the Global Alliance for Responsible Media (GARM) has highlighted gaps in the current approach.

It states how advertisers' “defensive” approach to improving suitability through overly restrictive keywords results in losses of “potentially millions of impressions” and may exclude potentially suitable content.

TV advertisers are used to knowing exactly where their ad will run, giving them total brand safety and suitability assurances. Digital platforms have attempted to compete by enabling tools to prevent ads running against dangerous content but cannot guarantee safety in the same way.

Smart suitability claims to be the solution with its balance between relevance and risk, including placing ads against content that may not seem obvious but can improve campaign performance. However, this requires alignment between advertisers, media owners, and platforms – a challenge due to strained relationships among key stakeholders.

Media owners need to improve taxonomies and packaging to help advertisers identify relevant placements, enhancing both ad relevance and revenue.

Full article on AdExchanger

Facebook Adds New Brand Safety Tools

Facebook (now Meta) announced a new brand suitability verification tool to help advertisers control ad placements, specifically avoiding topics like News and Politics, Social Issues, and Crime & Tragedy.

Amid declining younger user engagement, Meta’s move aims to retain ad publishers by supporting premium outlets and increasing CPMs.

Full article on Campaign

Audience Development

Contextual Storytelling Used to Overcome Skippable Culture

Contextual targeting alone is no longer enough to engage young audiences, with 82% of Gen Z skipping ads. According to MarTech, delivering an “elevated user experience” is crucial.

Brands are addressing this challenge by personalizing ads and collaborating with creators to produce bespoke content for specific channels or contexts. This hyper-targeted approach enhances engagement and supports brand campaigns in an era of scrolling and skipping.

Full article on MarTech Series

Measurement

Ad Spend SOV% Influenced by Performance Metrics

As reported by Digiday, advertisers are increasingly using performance metrics to determine ad spend. Publishers must shift from traditional CPM and CPV metrics to focus on retention and performance-based measures.

Media owners can enhance relevance by assessing portfolio performance and enabling transactions based on viewability or retention.

Full article on Digiday

OMG Using Attention Metrics to Plan Media

Omnicom Media Group is integrating attention metrics into media planning, shifting beyond post-campaign analysis. Amplified Intelligence’s CEO calls attention the “metric of the moment,” with video ad engagement measured through view duration becoming a key metric in determining media value.

Full article on Digiday

If you liked that why not take a look

What Is YouTube Monetisation Rate? Why It Matters More Than Views

YouTube views don't equal revenue. Monetisation rate measures the gap between views and earnings. Here's how to track and improve it across a portfolio.

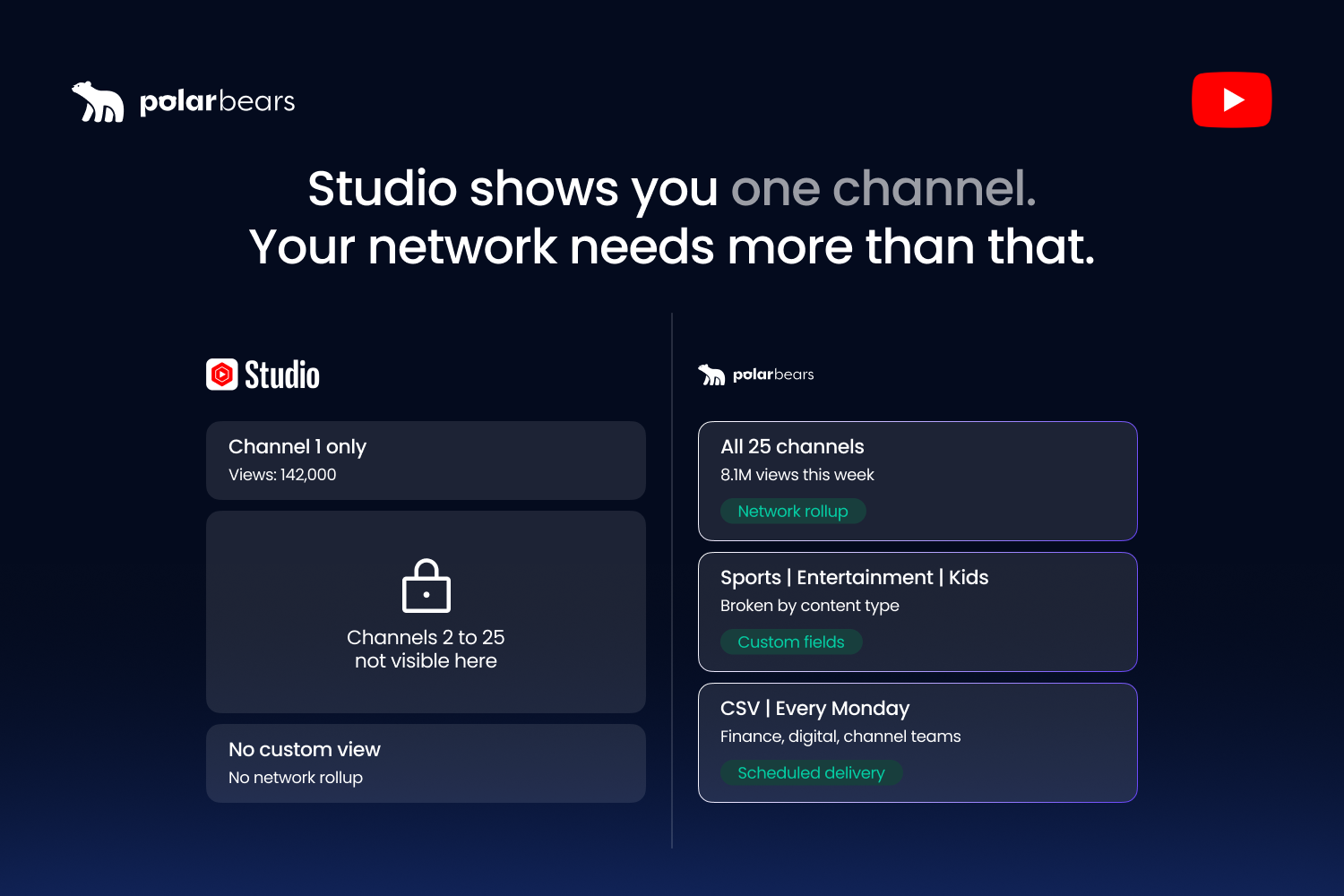

YouTube Content Categorisation at Scale: How Brands Group Content the Way Their Business Actually Runs

YouTube Studio organises content for viewers. Brands need to organise content for finance, sales, and rights. Here's how to bridge the gap.

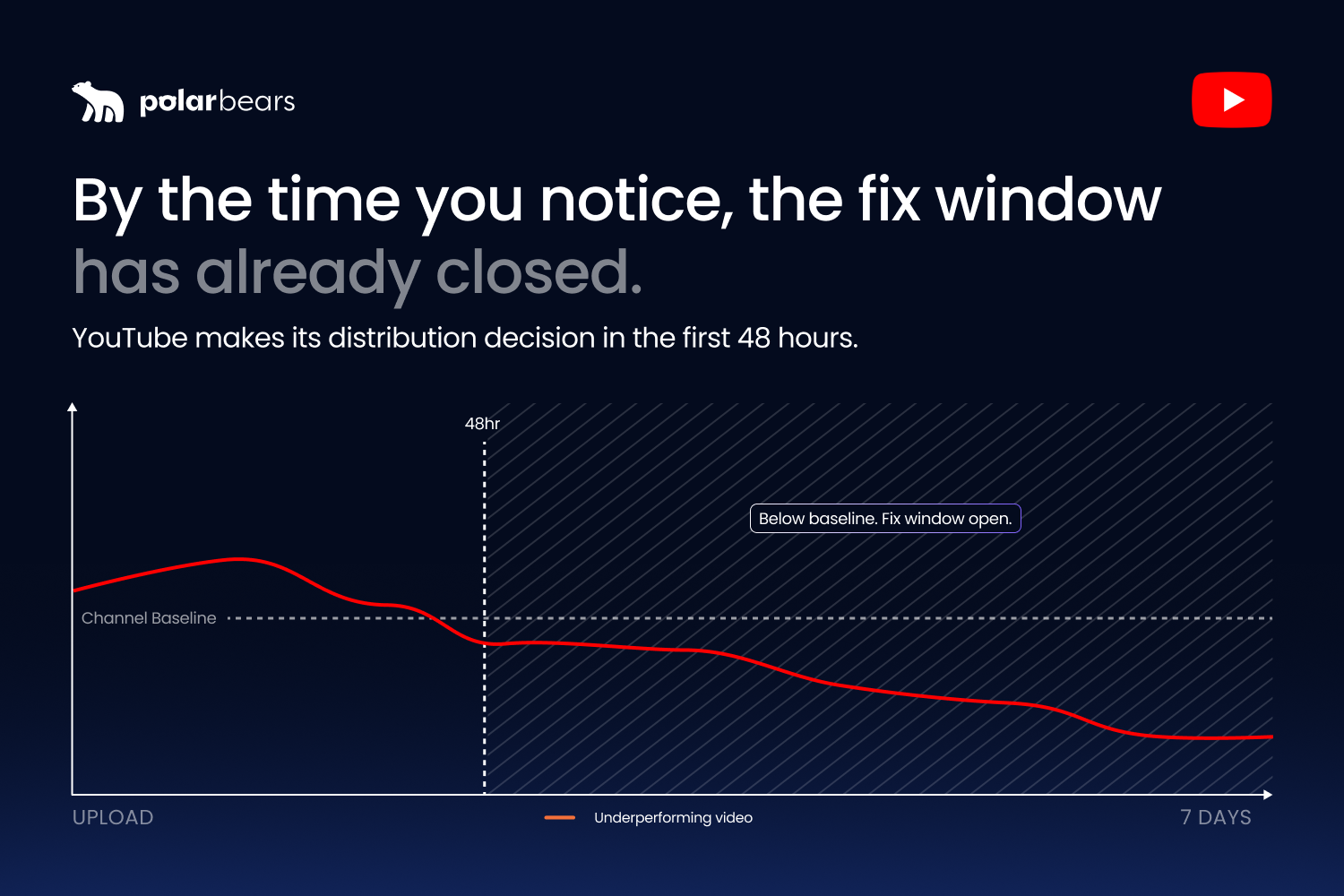

Early YouTube Performance: Which First-Week Metrics Actually Predict Revenue

A YouTube video's first 48 hours don't decide everything, but they decide more than most teams realise. Here's which early metrics actually predict 12-month revenue.

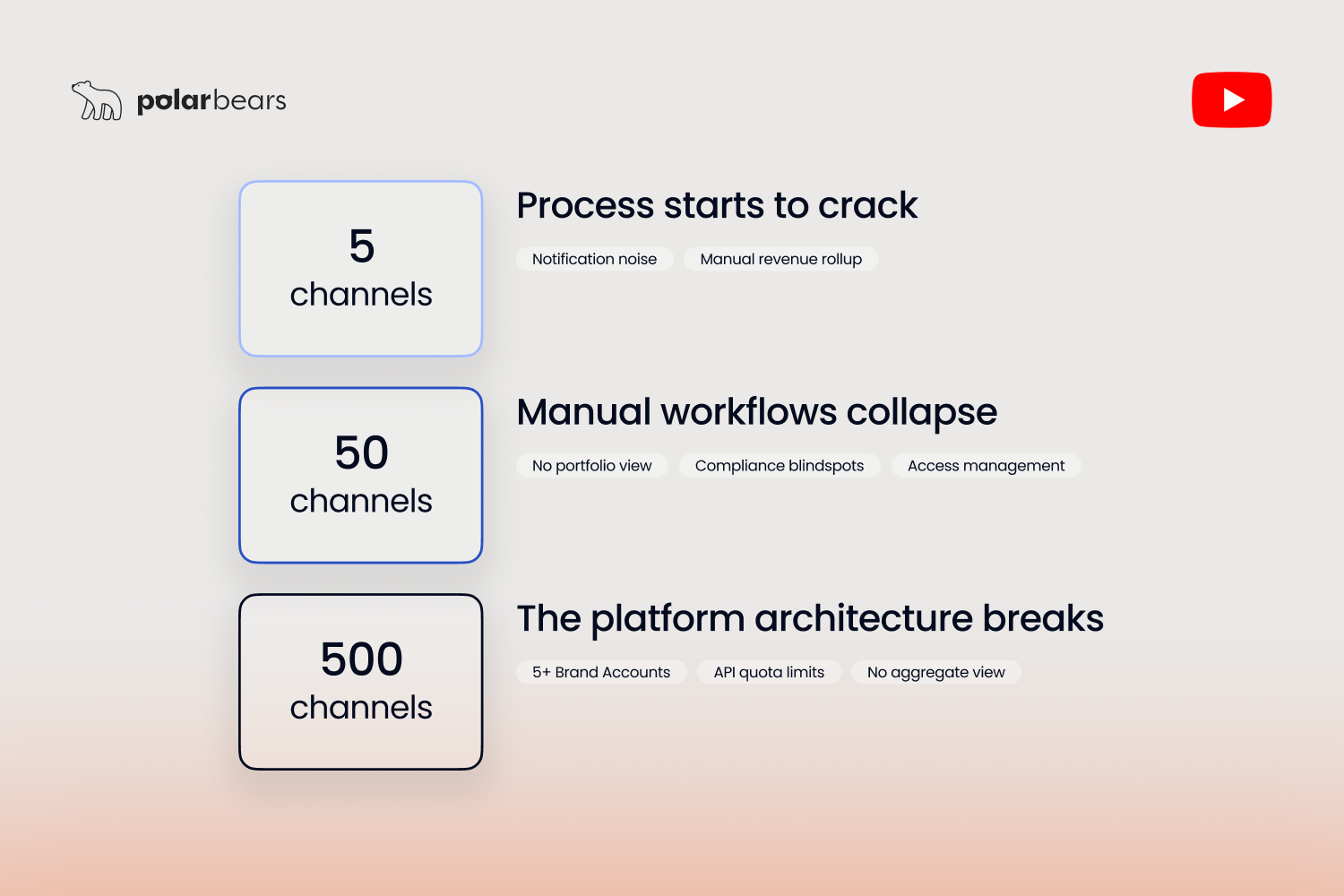

YouTube Studio Limits at Scale: What Breaks at 5, 50, 500 Channels

YouTube Studio is built for one channel at a time. Here's what breaks at 5, 50, and 500 channels, plus what to do about it.

Multi-Channel YouTube Reporting Without a CMS: Ops for Networks with 5+ Channels

Most brands managing 5+ YouTube channels can't get CMS access. Here's how to build multi-channel reporting that works regardless.

How to Catch Underperforming YouTube Videos Before They Cost You Revenue

Most YouTube videos either move in the first 48 hours or never do. Here's how to spot underperformers fast and decide what to fix.

Ready to maximise your YouTube revenue?

Get in touch and let’s begin exploring your channel’s hidden potential.